What Microsoft's Claude Decision Signals for AI Budgets

This month, Microsoft began phasing out many of its internal Claude Code licences in favour of GitHub Copilot CLI. Uber executives publicly admitted the company exhausted its planned 2026 AI tooling budget within four months, while struggling to clearly connect rising token spend to measurable product outcomes. Across the industry, AI software costs on major platforms have risen 20% to 37% in the past six months as vendors shift from flat-rate access toward usage-based pricing, where costs scale directly with usage.

The subsidy era of AI is ending. For most growth-stage companies, that's less a reason to reduce AI investment than a signal to manage what you're already spending on your AI operations more deliberately.

What Is Actually Happening in the Market Now

The flat-rate pricing that accelerated early enterprise AI adoption was never built for sustained, production-scale usage. As inference demand rises and agentic workflows dramatically increase compute consumption, AI providers are shifting toward pricing models that align revenue more closely with the real cost of operating large-scale AI systems.

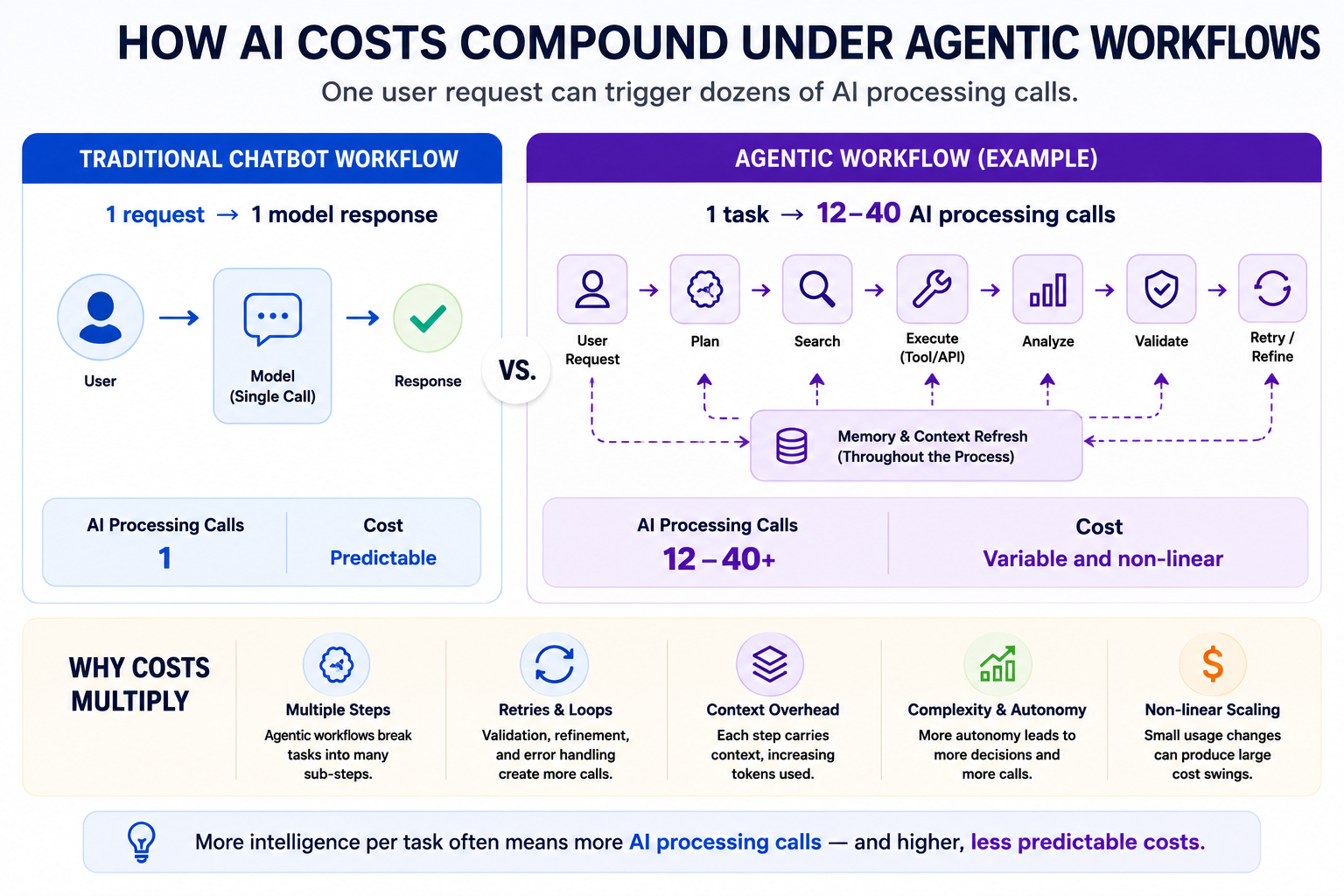

That shift is being driven by how AI usage itself is evolving. Many companies initially modelled costs around chatbot-style interactions: one request in, one response out. But agentic workflows can generate dozens of inference calls per task through planning, retrieval, tool use, validation, and retries, materially changing the cost structure behind AI operations.

For Series A and B companies embedding AI into marketing, finance, and operations functions, that shift has a direct bearing on how the next twelve months of operating expenses should be modelled, and on how those expenses read to an investor. A cost line that grew under flat-rate pricing and hasn't been remodelled against usage-based rates will likely understate forward spend, and that gap tends to surface at the worst possible moment.

Microsoft illustrates something important here: scale does not insulate a company from AI cost scrutiny. Microsoft invested $13 billion into OpenAI, owns the Azure infrastructure supporting much of the AI ecosystem, and has more leverage with AI vendors than almost any enterprise customer. If token-based billing and rising usage costs are forcing tooling reassessments even there, the same calculus is worth working through for every company running AI at meaningful volume.

Uber's situation points to a different but related issue. The spend was real. The link back to a measurable business outcome was less clear. That is a financial governance gap that becomes highly visible when a CFO, board member, or investor asks for the return on an AI budget line and it becomes more visible, not less, as AI spend grows.

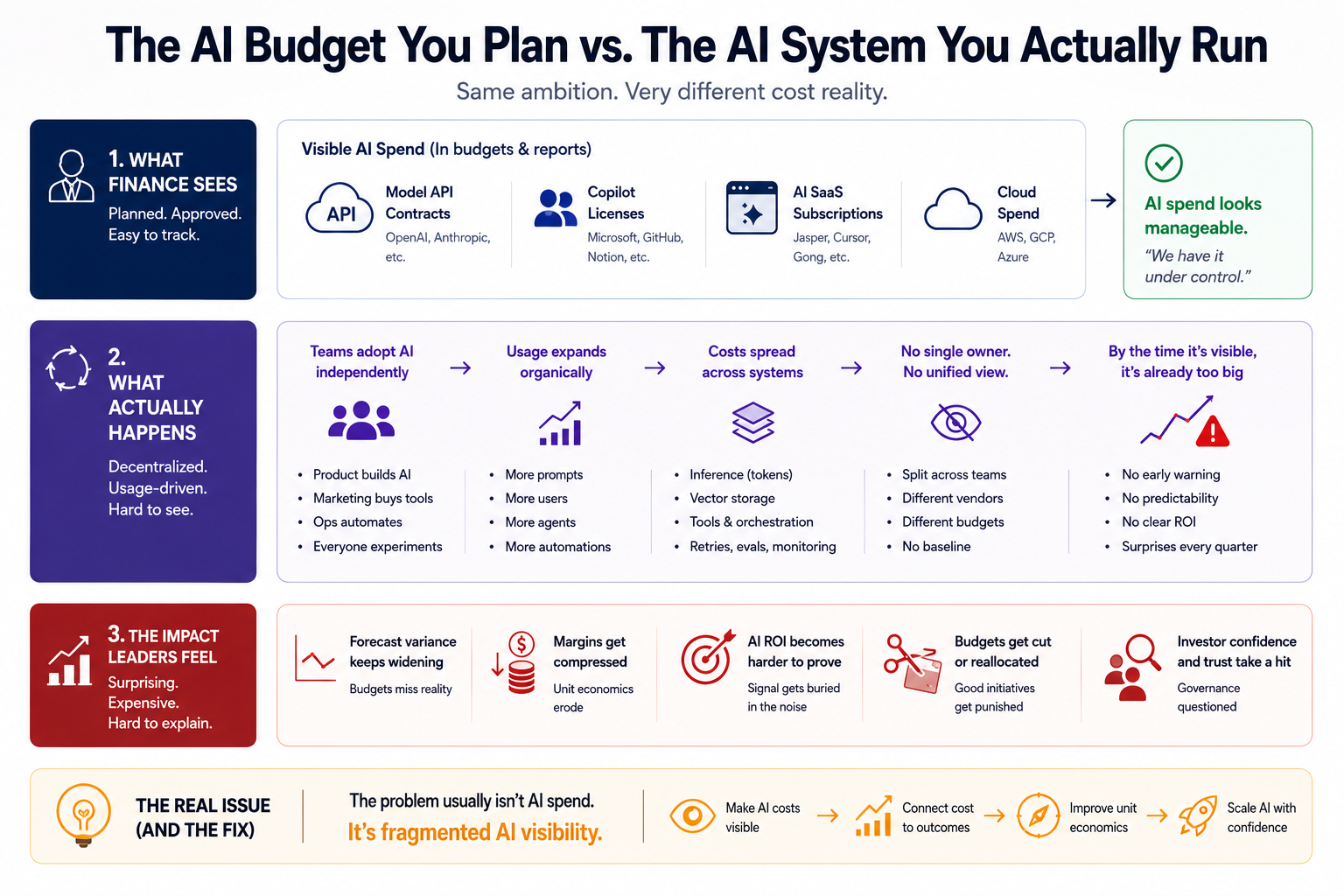

Is Your AI Budget Larger Than What Your Financial Model Reflects?

Most Series A and B companies are running multiple distinct AI cost streams — copilots, inference APIs, embedded SaaS AI features, agentic background workflows — with few of them tracked against each other. AI adoption happened department by department, which means the cost structure has grown organically rather than by design.

Finance teams are typically tracking what's invoiced: licences, subscriptions, a handful of API cost lines. That captures the visible layer. What it often misses is the inference consumption embedded across those tools: the API calls generated by agentic workflows, the token usage accumulating inside platforms that bill it as a single line, the background automations that don't produce a discrete cost event. Under usage-based pricing, that layer is where cost growth is actually happening.

That invisibility was manageable when pricing was flat. Under usage-based pricing, it's where the forecast gap lives. The companies most exposed aren't the ones spending the most on AI. They're the ones whose finance function has the least visibility into what's actually driving the number. The question for a CFO approaching a raise isn't whether this gap exists — for most growth-stage companies it does. It's whether it gets addressed before an investor looks at the cost line or after.

Signs Your AI Spend Has Outgrown Your Financial Model

- Growth in spend without growth in output: AI spend is growing faster than headcount or revenue. If the AI budget line is expanding while the team and top line stay roughly flat, usage is scaling in ways the business hasn't deliberately decided to scale it. That's worth understanding before a raise, because an investor will ask.

- Costs moving without a clear cause: Token usage spikes without a clear revenue correlation. A month where inference costs jump significantly should map to something — a campaign push, a product launch, a new workflow going live. If it doesn't, there's no visibility into what's driving consumption.

- No central view on model selection: Teams are selecting models independently. When engineering, marketing, and operations are each choosing AI tools without a central view, the business is likely running frontier-tier models on tasks that don't require them — and paying the cost difference at scale.

- AI modelled as SaaS when it runs like infrastructure: Finance is forecasting AI as a fixed cost. If the forward model treats AI spend as a stable line rather than a variable infrastructure cost that scales with workflow volume, it will understate forward spend as agentic usage grows.

- Inference spend with no owner: There is no owner for inference efficiency. Cloud infrastructure has a cost owner. Data warehousing has a cost owner. For most growth-stage companies, AI inference spend doesn't. That gap becomes a diligence question as the number gets larger.

How much confidence do you have that your AI cost forecast reflects what's actually happening across the business—not just what's showing up on invoices?

What Your AI Cost Line Says to an Investor in the Data Room

What we see consistently on the investor side is this: AI cost structure has become a proxy for financial governance discipline, in the same way cloud infrastructure cost management became a signal of operational maturity five years ago.

An investor reviewing a data room today isn't just asking whether AI spend is justified. They're asking whether the CFO can account for every dollar of it across the business, model it forward against actual workflow volume rather than historical licences, and connect it directly to the ARR growth, burn efficiency, or headcount leverage the raise narrative is built on. A management team that can answer those questions in the room (without pulling numbers from three different people) signals something that goes beyond AI.

What we see on the founder and operator side is that most growth-stage companies aren't structured to answer those questions yet. Not because the finance team is behind, but because AI cost governance hasn't been treated as an infrastructure discipline in the same way cloud or data has. The spend is real and growing. The consolidation, ownership, and attribution layer often isn't there.

These are the four questions most likely to come up in the data room and worth having a clean answer to before the conversation starts:

- What is the total AI spend across the business, with a single owner and a consolidated view?

- How does that spend scale as revenue grows — does the model reflect usage-based pricing or flat-rate assumptions that no longer hold?

- Which AI investments are directly attributable to the commercial outcomes driving the valuation narrative — pipeline growth, reduced cost per acquisition, faster close cycles?

- And has the forward model been updated to reflect current per-token pricing across the platforms the business actually runs on?

By the time a raise is in motion, the data room is already built. The AI cost line in it reflects decisions, or the absence of them, made months earlier.

Three Things Worth Having in Place Before Your Next Raise

Finance functions that move through Series B diligence cleanly on AI cost tend to have these things in place:

A consolidated spend view. AI costs distributed across department tool budgets without a single consolidated number and clear ownership will look like a gap in financial governance. Start by pulling every line item with an AI vendor name against it — API costs, SaaS subscriptions, copilot licences, cloud inference spend — into a single view. Assign one owner. That number is your baseline.

An attribution framework. Connecting AI spend to the commercial outcomes it is expected to influence (i.e., ARR growth, burn efficiency, headcount leverage) transforms a cost line into an investment with a measurable return. The framework doesn't need to be complex. It needs to exist and be consistent with how the business reports on other operational investments.

A forward cost model based on usage, not licence history. Under usage-based pricing, forward AI cost scales with workflow volume, not with the number of seats in the tool. The reforecast is worth doing before the raise is in motion.

The faster a business scales, the more moving parts its AI cost structure tends to have. The finance functions that stay ahead of it tend to have a partner who has built this infrastructure before and who understands what it needs to look like from both sides of the table

If a raise is coming and your AI cost structure isn't ready, let's connect today to discuss.

.png)

.webp)

%20Is%20Telling%20Investors%20a%20Story.webp)

.webp)